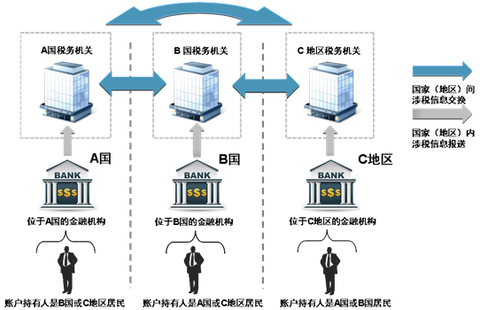

In order to fulfill the international obligation of automatic exchange of tax-related information in financial accounts, and to regulate the financial institutions' due diligence on tax-related information of non-resident financial accounts, the State Administration of Taxation, the Ministry of Finance, the People's Bank of China, the Bank of China 601988, the Stock Bar Supervision Committee, China Securities The Supervisory Management Committee and the China Insurance Regulatory Commission have formulated the Measures for the Administration of Due Diligence of Tax Information on Non-Resident Financial Accounts (hereinafter referred to as the “Administrative Measuresâ€). The relevant contents of the "Administrative Measures" are as follows: 1. What is the background of the "Administrative Measures"? Entrusted by the G20, the Organisation for Economic Co-operation and Development (OECD) issued the standard for the automatic exchange of tax-related information in financial accounts (hereinafter referred to as “standardsâ€) in July 2014, which was approved by the G20 Brisbane Summit. It provides a powerful information tool for countries to strengthen international tax cooperation and combat cross-border tax evasion. Under the strong promotion of the G20, 100 countries (regions) have pledged to implement the “standardsâ€. With the approval of the State Council, China has promised to implement the “standard†to the G20. The first time for exchanging information for the first time is September 2018. In July 2015, the Multilateral Tax Administration and Mutual Assistance Convention was approved by the 15th meeting of the Standing Committee of the 12th National People's Congress. It entered into force for China in February 2016 and laid a multilateral legal foundation for the implementation of the “standards†in China. In December 2015, the State Administration of Taxation signed the Agreement on Multilateral Competent Authorities for the Automatic Exchange of Tax Information Related to Financial Accounts, which provided an operational basis for the exchange of tax information on financial accounts between China and other countries (regions). The "Management Measures" issued this time aims to translate the internationally accepted "standards" into specific requirements for adapting to China's national conditions, and provide legal basis and operational guidelines for the implementation of "standards" in China. This is not only an important measure for China to actively promote the implementation of "standards". It is also a concrete manifestation of China’s fulfillment of its international commitments. Second, what is the main content of the "standard"? The “standard†consists of two parts: the agreement between the competent authorities and the unified reporting standard. The Inter-Government Agreement is an operational document that regulates the automatic exchange of tax-related information in financial accounts between tax authorities in each country (region). The Uniform Reporting Standard sets out the requirements and procedures for financial institutions to identify, collect and report non-resident personal and institutional account information. According to the "standard", the financial account is automatically exchanged for tax information. First, a country (region) financial institution uses the due diligence procedure to identify the account of another country (region) tax resident individual and enterprise opened by the financial institution. The competent authority of the country (region) where the financial institution is located submits the account holder's name, taxpayer identification number, address, account number, account balance or value, interest, dividends, and income from the sale of financial assets (excluding physical assets), etc. The country's (regional) tax authorities exchange information with the account holder's resident tax authorities, and ultimately provide information support for countries (regions) to conduct cross-border tax source supervision. The specific process is shown in the following figure: 3. What is the relationship between the “standards†and the US “Overseas Account Tax Compliance Actâ€? In 2010, the United States enacted the Foreign Account Tax Compliance Act (FATCA), which requires foreign financial institutions to report information about US tax residents (including US citizens, green card holders) accounts to the US Internal Revenue Service, otherwise foreign financial institutions are receiving A punitive withholding tax of 30% will be withheld when a specific income is derived from the United States. FATCA mainly adopts the bilateral information exchange mechanism, that is, the United States and other countries (regions) exchange information according to bilateral intergovernmental agreements. The "standard" is a multilateral information exchange system designed based on the FATCA Intergovernmental Agreement. It can be said to be the global version of FATCA. The “standard†is roughly the same as the content of FATCA, but there are some differences in the details, including the object of submission, the due diligence threshold of the individual account, the type of financial institution exempt from submitting information, and the punishment measures. The Administrative Measures are intended to identify non-resident accounts required by the Standard and do not apply to US tax resident accounts as required by FATCA. In view of the fact that our government is actively negotiating with the US government about the FATCA intergovernmental agreement, financial institutions may consider coordinating “standards†with FATCA at the operational level, including integrating the declaration documents of the two according to their own business needs. 4. Which countries (regions) have committed to implement the “standardsâ€? 50 countries (regions) that exchanged information for the first time in 2017 Anguilla, Argentina, Belgium, Bermuda, British Virgin Islands, Bulgaria, Cayman Islands, Colombia, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Faroe Islands, Finland, France, Germany, Gibraltar, Greece, Greenland, Roots West Island, Hungary, Iceland, India, Ireland, Isle of Man, Italy, Jersey, South Korea, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Mexico, Montserrat, Netherlands, Norway, Poland, Portugal, Romania, San Marino, Seychelles, Slovakia, Slovenia, South Africa, Spain, Sweden, Turks and Caicos Islands, United Kingdom 50 countries (regions) that exchanged information for the first time in 2018 Andorra, Antigua and Barbuda, Aruba, Australia, Austria, Bahamas, Bahrain, Barbados, Belize, Brazil, Brunei Darussalam, Canada, Chile, China, Cook Islands, Costa Rica, Curaçao, Dominica, Ghana, Grenada, Hong Kong, China, Indonesia, Israel, Japan, Kuwait, Lebanon, Marshall Islands, Macau, Malaysia, Malaysia, Mauritius, Monaco, Nauru, New Zealand, Niue, Panama, Qatar, Russia , Saint Kitts and Nevis, Samoa, Saint Lucia, Saint Vincent and the Grenadines, Saudi Arabia, Singapore, Saint Martin, Switzerland, Trinidad and Tobago, Turkey, United Arab Emirates, Uruguay, Vanuatu It is expected that more countries (regions) will commit to implementing “standards†in the future. For countries (regions) that have not promised to implement “standardsâ€, the international community may adopt joint countermeasures to promote its commitment to implement “standards†and increase tax transparency. In the long run, the implementation of “standards†on a global scale is the general trend, and the automatic exchange of tax information in financial accounts will eventually cover most countries (regions). 5. Which countries (regions) will China exchange financial account tax information with? Countries (regions) that have committed to implement “standards†mutually select information exchange partners, and both parties have the intention to establish partnerships. China will establish information exchange partnerships with as many countries as possible. For related information, please refer to the website of the State Administration of Taxation. 6. What are the principles for formulating the Administrative Measures? First, strictly follow international standards. The “standards†developed by the OECD and the G20 member states have become the new international standard for tax transparency. In order to build a good international tax collection order and avoid the uneven implementation level of countries (regions), the international community requires countries (regions) to strictly abide by the "standards" in the process of domestic law transformation, and will International review of development and implementation. Therefore, the “Administrative Measures†are formulated in accordance with the main contents of the “Standardsâ€, which stipulate the principles and procedures for the identification of non-resident accounts and the collection of relevant information by domestic financial institutions, including the interpretation of basic definitions, the due diligence procedures for individual accounts and institutional accounts. The range of information that financial institutions need to collect and report. The second is to fully consider the domestic reality. Considering that the contents of the “Administrative Measures†involve the daily compliance work of financial institutions and the personal experience of financial institution clients, the “Administrative Measures†have repeatedly sought the opinions of the financial industry through the financial authorities, and in October 2016 at the State Administration of Taxation. The website is open to the public for comments. In line with the principle of taking into account both international and domestic needs, the “Administrative Measures†have considered the demands of domestic parties as far as possible within the scope of “standardsâ€, thereby reducing the compliance burden of financial institutions and the impact on customer experience. 7. What is the impact of the Administrative Measures on the public? The "Administrative Measures" have little impact on the public, and they have a certain impact on some individuals and institutions that open new accounts in financial institutions. From July 1, 2017, individuals and institutions will open new accounts in financial institutions, including opening a deposit account in a commercial bank and purchasing commercial insurance at an insurance company. An application for opening an account or an additional declaration document must be required at the financial institution's request. Declare its tax resident status. Since most of the individuals and institutions that open accounts in China's domestic financial institutions are Chinese tax residents, it is only necessary to check the “Chinese tax residents†when filling out the declaration documents. The experience of opening an account is not significant. If the above-mentioned individuals and institutions have already opened accounts in the previous period, when a new account is opened in the same financial institution after July 1, 2017, in most cases, no tax resident status statement is required, and the tax resident status is retained by the financial institution based on the retained information. To confirm. For accounts that have been opened before July 1, 2017, the financial institution confirms the tax resident status of the account holder based on the retained information, and a very small number of unidentified individuals and institutions need to cooperate with the materials provided. 8. Who is the main influence of the Administrative Measures? The "Administrative Measures" mainly affects non-residents who open accounts in China or passive non-financial institutions that have non-resident controllers. The term "non-residents" as used herein refers to individuals and enterprises other than Chinese tax residents (including other organizations), but does not include government agencies, international organizations, central banks, financial institutions, or companies listed and traded on the securities market recognized and regulated by the local government. And its affiliates. Non-residents or passive non-financial institutions with non-resident controllers need to fill in the tax resident identity statement documents of the account holder or controller in detail when opening a financial account, including name (name), current address, and tax resident country. (Region), resident country (region) taxpayer identification number, place of birth, date of birth, etc., and should ensure that the information is true and accurate. After the above information is reported to the relevant department, it will be exchanged by the State Administration of Taxation in accordance with the agreement signed by China to the account holder's resident tax authority. 9. What is a negative non-financial institution? If the majority of the income of a non-financial institution is income from negative operating activities such as dividends, interest, rent, royalties, etc., the institution is a passive non-financial institution, such as a tax haven, holding only the equity of the subsidiary. Intermediate holding company. Since passive non-financial institutions are easily used as tools for cross-border tax evasion, financial institutions need to identify these institutions and the actual controllers behind them. If the controller of a negative non-financial institution is a non-resident, the financial institution needs to collect and report information about the controller. 10. Why do account holders need to fill out a tax resident identity statement? The “Administrative Measures†adopts the concept of tax residents, which is different from the concept of residents in the residence management regulations. Tax resident identification standards are complex and cannot be directly determined by ordinary resident identity documents. Therefore, individuals and institutions that need to open accounts must declare their tax resident status. Individuals and organizations that open accounts should cooperate with the due diligence work of financial institutions, fill in the tax resident identity statement documents in a true, timely, accurate and complete manner, provide relevant materials as stipulated in the Administrative Measures, and bear the consequences arising from non-compliance with regulations. Legal liability and risk. 11. How does the account holder judge his or her tax resident status? The criteria for the identification of tax resident status in national laws of countries (regions) are not consistent. For individuals, the standard of residence (residence) and the standard of residence time are usually adopted at the same time. Taxpayers can form tax residents of the country as long as they meet one of them. For enterprises, the registration standards and management institutions are usually adopted. Location standard. Take China as an example. According to China's tax law, a Chinese tax resident individual refers to an individual who has a domicile in China or has lived in the territory for one year without a residence (having a domicile in China refers to habituality in China due to household registration, family, and economic interests). Residents; Chinese tax resident enterprises refer to enterprises (including other organizations) established in China according to law or established in accordance with foreign (regional) laws but with actual management institutions in China. Account holders should make a comprehensive judgment on their tax resident status according to their actual conditions and the relevant national (regional) tax resident identification rules. The SAT website will publish relevant information for reference by financial institutions and account holders (http://). Account holders can also consult a professional tax advisor to determine their tax resident status. 12. Will the account information of Chinese tax resident individuals be reported and exchanged? If the account holder is a Chinese tax resident individual, the financial institution will not collect and submit relevant account information, nor will it be exchanged to other countries (regions). If the account holder also constitutes a Chinese tax resident and other national (regional) tax residents, the account information in China will be exchanged with the tax authorities of the corresponding tax resident country (region), and the overseas account information will be exchanged with the State Administration of Taxation. . 13. What is the due diligence referred to in the Administrative Measures? The due diligence referred to in the Administrative Measures is not a general investigation. It refers to the financial institution's understanding of the tax resident status of the account holder or the relevant controller in accordance with the prescribed procedures, identifying non-resident financial accounts, collecting and recording relevant account information. For a long time, financial institutions have carried out similar customer identification work for the purpose of anti-money laundering at the request of relevant authorities, laying the foundation for the implementation of the "Administrative Measures." 14. Which financial institutions need to conduct due diligence in accordance with the Administrative Measures? Financial institutions as defined in the Administrative Measures are not the same as financial institutions that are understood in ordinary economic life. For example, a company belongs to the “financial industry†according to the national economic industry classification, but it does not necessarily belong to the financial institution referred to in the “Administrative Measuresâ€. Financial institutions such as deposit institutions, custodian institutions, investment institutions and specific insurance institutions established within the territory of China shall conduct due diligence in accordance with the provisions of the Administrative Measures. The relevant definitions are specifically explained and enumerated in the Administrative Measures. Financial asset management companies, finance companies, financial leasing companies, auto finance companies, consumer finance companies, currency brokerage companies, securities registration and settlement institutions, and other non-eligible institutions are not financial institutions under the Administrative Measures. Conduct due diligence. 15. Which accounts are within the scope of due diligence as stipulated in the Administrative Measures? From July 1, 2017, domestic financial institutions will conduct due diligence on deposit accounts, escrow accounts, equity interests or creditor rights of investment institutions, and insurance contracts or annuity contracts with cash value. These accounts, regardless of the amount of money, should be used to identify whether the account holder is a non-resident through due diligence. In practice, some financial accounts are used to evade taxes at a lower risk. Therefore, the Administrative Measures also provide for exemption from due diligence in accordance with international standards, such as eligible pension accounts and social security. Accounts, term life insurance contracts, dormant accounts, and other eligible accounts. Relevant conditions are specified in the Administrative Measures. 16. Is the due diligence procedure for all categories of accounts the same? The Administrative Measures divides accounts into two types of accounts, personal and institutional. Each type of account is divided into new open accounts and stock accounts. The due diligence requirements and procedures for different categories of accounts vary. To put it simply, the new account opening due diligence requirements are relatively strict, requiring the account holder to provide their tax resident status statement documents, and the financial institution conducts a reasonable review based on the account opening information. The stock account due diligence process is relatively simple, and financial institutions mainly rely on retained data for retrieval. Conditional financial institutions may choose to apply the new account due diligence requirements to the stock account. The specific requirements are detailed in the following table: Account category description Due diligence procedure time requirement personal Newly opened Open after 2017.7.1 Statement file + reasonableness review 2017.7.1 Start Stock Low net worth As of 2017.6.30, the total balance of the account is $1 million. Retrieve retained data (electronic) Completed 2018.12.31 High net worth As of 2017.6.30 account total balance > 1 million US dollars Retrieve retained data (electronic + paper) + ask account manager 2017.12.31 completed mechanism Newly opened Open after 2017.7.1 Statement file + reasonableness review 2017.7.1 Start Stock Small amount As of 2017.6.30, the total balance of the account is $250,000. No need to deal with no other As of 2017.6.30 account total balance > 250,000 US dollars Retrieve retained data + partial account statement file Completed 2018.12.31 17. What preparations do financial institutions need to perform? In order to implement the Administrative Measures, financial institutions should establish a complete non-resident financial account due diligence management system, design reasonable business processes and operational specifications, and complete the development and transformation of relevant information systems. Financial institutions also need to strengthen the training of staff in relevant positions of the institution, so that they have the awareness and ability to conduct due diligence on non-resident financial accounts. In addition, financial institutions can also publicize their customers by printing publicity materials, so that they can understand the relevant background of the Administrative Measures and cooperate with financial institutions to complete due diligence work. It should be noted that financial institutions should register on the website of the State Administration of Taxation (http://) before December 31, 2017 to prepare for the next information report. . 18. Can a financial institution entrust other agencies to perform due diligence obligations? Financial institutions may entrust third parties to perform due diligence obligations, but the relevant responsibilities are still borne by financial institutions. Where funds, trusts, etc. are investment institutions, fund management companies and trust companies may be used as third parties to complete due diligence related work. Where a financial institution entrusts other institutions to sell financial products to customers, the agency shall cooperate with the entrusting agency to conduct due diligence and provide information to the entrusting agency for submission. In order to ensure the implementation effect, financial institutions should properly keep the information collected during the due diligence process for a period of at least five years. 19. What are the follow-up measures for the “Administrative Measuresâ€? Relevant departments will formulate supporting information reporting requirements for financial institutions, and clarify the channels, formats and relevant technical specifications, so that financial institutions can report the information collected through due diligence to relevant departments. In order to facilitate financial institutions and the public to have an in-depth understanding of the automatic exchange of tax information on financial accounts, a special website (http://) will be opened on the website of the State Administration of Taxation. The data, including the tax resident identification rules of various countries, the taxpayer identification number coding rules, and common problems, are used for reference by financial institutions and the public. 20. Will customer privacy be revealed? The collection and reporting of non-resident account information by financial institutions will not result in the disclosure of customer information. First, the "Administrative Measures" stipulate that financial institutions should strictly keep confidential customer information. Second, financial institutions are obliged to fully explain to customers the information collection and reporting obligations they need to perform, and will not collect account information without the customer's knowledge. Third, relevant departments should keep customer information confidential according to regulations. Fourth, the tax authorities of the two countries exchange information through a secure and encrypted unified transmission system. Fifth, the customer information submitted by financial institutions is only used for tax collection purposes in principle. 21. Does the exchange of information mean increasing the tax burden of taxpayers? The automatic exchange of tax-related information in financial accounts is a means of strengthening cross-border tax source management between countries (regions) and will not increase the tax liability that taxpayers should perform. The information exchanged is from third-party information from abroad, and is mainly used for risk assessment in various countries, and is not directly used for taxation. For taxpayers who are assessed as high risk, the tax authorities will conduct targeted tax inspections and take appropriate follow-up management measures. Taxpayers who file tax returns in good faith do not have to worry about increasing the tax burden due to information exchange. 22. What is the impact on overseas Chinese and overseas Chinese? Overseas Chinese who open new accounts in financial institutions in China should provide financial institutions with personal tax resident status declaration documents when opening an account. If an overseas Chinese who has already opened an account with a financial institution in China has a non-resident identity such as an overseas address or telephone number, the account holder must cooperate with the financial institution to confirm whether it is a non-resident. For overseas Chinese who are confirmed as non-residents, the financial institution will collect and submit account information, which will be exchanged by the State Administration of Taxation to the taxation authority of the tax resident country; if it is confirmed as a Chinese tax resident, the relevant account information will not be collected and exchanged. Overseas Chinese with financial accounts outside China, if the country (region) is also implementing “standardsâ€, overseas Chinese must cooperate with local financial institutions to confirm their tax resident status. For overseas Chinese who are recognized as Chinese tax residents, the tax authorities of the country (region) where they are located will provide relevant account information to the State Administration of Taxation; if they are confirmed as tax residents of the country (region), the relevant account information will not be reported back to China. If the country (region) where the overseas Chinese are located does not implement the "standard", it will not be affected in most cases. However, if the person himself is the controller of an investment institution in the locality, then when the investment institution opens an account in the country where the “standard†is implemented, the financial institution of the other party will collect the information of the controller, that is, its own information. Twenty-three, what are the precautions for the individual residents of China to open an account abroad? Financial institutions established in countries (regions) that have committed to implement “standards†need to identify non-resident accounts and submit account-related information to the local tax authorities. When a tax resident individual opens a financial account in these countries (regions), he or she needs to provide tax resident identity information, including the taxpayer identification number of China. According to the relevant regulations of China, the taxpayer identification number is the resident ID number of the individual whose ID is valid. As financial institutions may need to verify the relevant documents of the account holders, please open my account with the resident ID card. For individuals who use foreign passports and other documents as valid identification, the taxpayer identification number rules can be found on the website of the State Administration of Taxation (http://). (Editor: HN666) Baseball Hat Cap,Baseball Cap Safety Hat,Cotton Baseball Caps,Breathable And Comfortable Sport Cap Jingjiang Pingdong Import&Export Co.,Ltd , https://www.socksjjpd.com